While popular, Tide Pods are staggeringly dangerous for young children and people with disabilities. Proctor and Gamble launched the Tide Pods in 2012. In 2011, 2,862 children were hospitalized because of laundry-detergent related injuries. In 2013, that number was triple: 9,004 children were driven to hospitals by laundry detergent. The problem isn’t that Tide Pods are uniquely toxic, or contain chemicals never used before. The problem is that they’re cute. They’re colorful. And they’re small. It’s the good things about Tide Pods that we have to change to make them safer. What Tide Pods teach us about consumer product safety is that it’s not always the “bad parts” of…

-

-

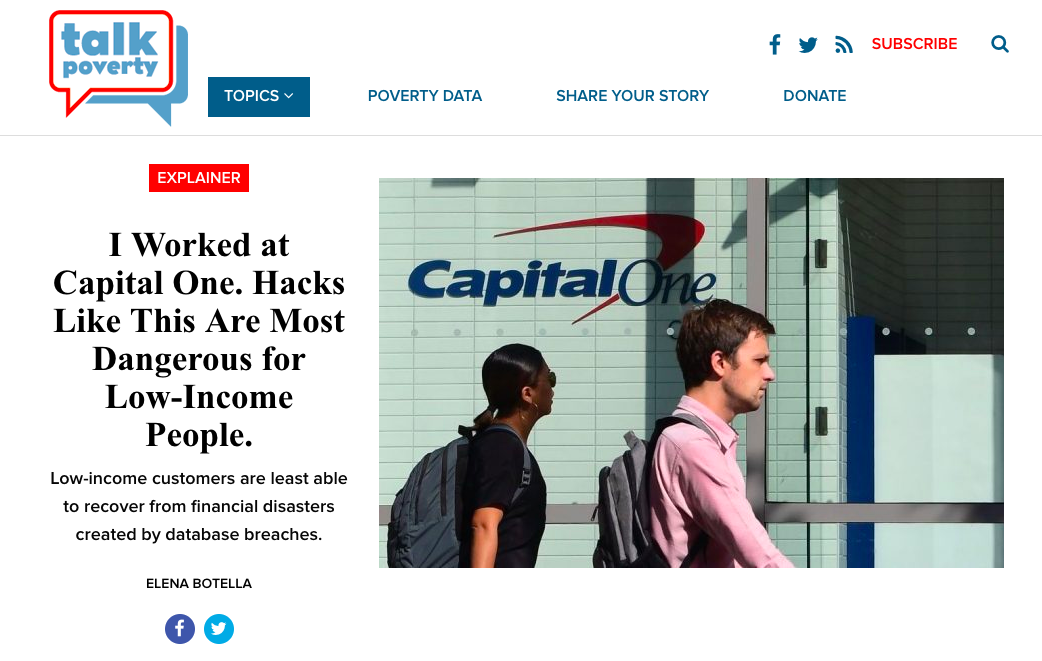

Two takes on the Capital One data breach

For TalkPoverty, a publication of the Center for American Progress, I wrote about the fact that the Capital One breach put Capital One’s secured card customers at the greatest risk. Secured cards give people who ordinarily wouldn’t be approved for credit a chance to put down a security deposit and get a credit card — but often at a high price, since 3 in 4 secured card customers end up carrying a revolving balance, paying late fees and interest rates of 25%+ to borrow what is effectively their own money. TalkPoverty: I worked at Capital One. Hacks like these are most dangerous for low-income people. On LinkedIn, I express the…

-

The space between want and need

I’m now on Day 13 on my road trip at my aunt and uncle’s farm in Blue Earth County, Minnesota — today is the first day of the planting season for corn. It’s getting a late start because of all the rain. My next stop will be in Iowa. If there’s one comment that has come up in most of my interviews with the people who wished they hadn’t borrowed money on a credit card, it’s that they used the card for things they realized they “didn’t really need.” That word “really” hints at the notion that there is actually a lot of ambiguous space in between want and need.…

-

Are credit card rewards even good for consumers?

Earlier this week, the Wall Street Journal reported that merchants like Home Depot, Target, and Amazon are becoming increasingly frustrated with the high fees they pay to accept rewards credit cards, and are seeking relief from the courts or through negotiations with Visa and Mastercard. Particularly, merchants are looking for the networks Visa and Mastercard to end their ‘honor all cards’ rules, which say that if you accept any Visa credit card you need to accept all Visa credit cards, and ditto with Mastercard. Today, if you spend $100 at a large grocery store, Visa would charge the store a $2.20 processing fee if you used a top-tier rewards credit…

-

“I’m not falling for your tricks” and other mixed reactions to credit limit increases

All it takes is a quick search on Twitter to see that credit limit increases drive incredibly strong and oftentimes mixed emotional reactions for Americans. To clarify, when I say ‘credit limit increase’ here, I’m talking about when a credit card issuer raises the limit of how much a customer is able to spend or borrow. In theory, having access to more credit — that you’re under no obligation to use — seems like it would be a strictly good thing. It’s there if you need it, and if you don’t use your higher credit limit, your credit score will typically go up (this article explains why). But clearly, many…