D.C. City Council held a hearing yesterday to consider overturning Initiative 77, which would gradually raise the tipped minimum wage for D.C. workers from $3.33 to $12.50, rising to $15 along with the base minimum wage in 2020.

Opponents of the Initiative claim to have the backing of not only the District’s restaurant owner and operators, but the city’s restaurant servers and bartenders as well. At yesterday’s hearing, Jill Tyler, Co-Owner of Michelin-starred restaurant Tail Up Goat in Adams Morgan said “by and large, the current system works,” resulting in workers “who can afford to buy a home, who can afford to raise a family,” noting that 40 of her 47 employees live in the District of Columbia, and nearly half live in Ward 1 where Tail Up Goat is located.

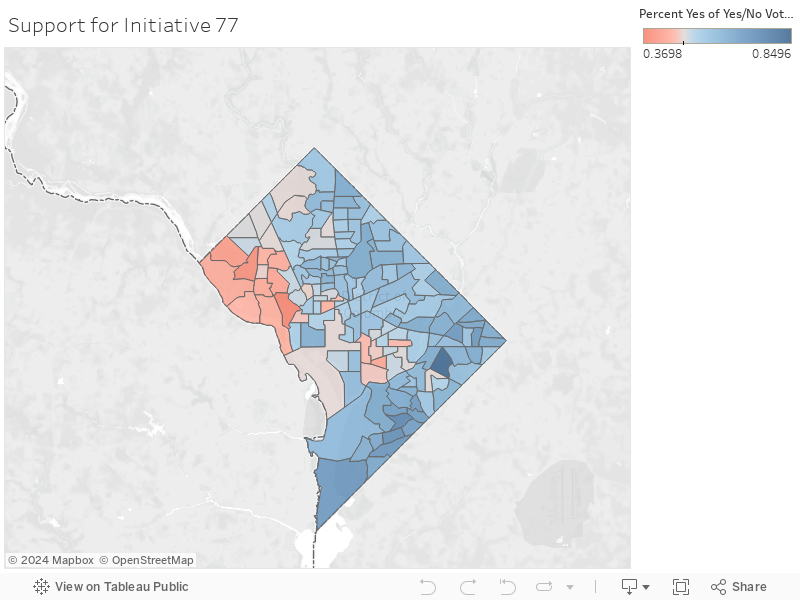

But supporters seeking to raise the tipped minimum wage state that many tipped workers have avoided speaking up publicly fearing retaliation from employers, and that those workers making poverty-level wages have less political and economic capital to make their voices heard. City Council Chairman Phil Mendelson noted “It’s hard for me to know what to do with the people who aren’t at the table.” But the easiest time and place for tipped workers to make their preferences was on Election Day itself, and while we don’t know how each person voted, it’s clear that the only neighborhoods that voted ‘No’ to raise the tipped minimum wage are the ones where very few restaurant workers live.

I matched U.S. Census Bureau data from the American Community Survey at the tract level with D.C. Board of Election data at the precinct level, and it tells a clear story.

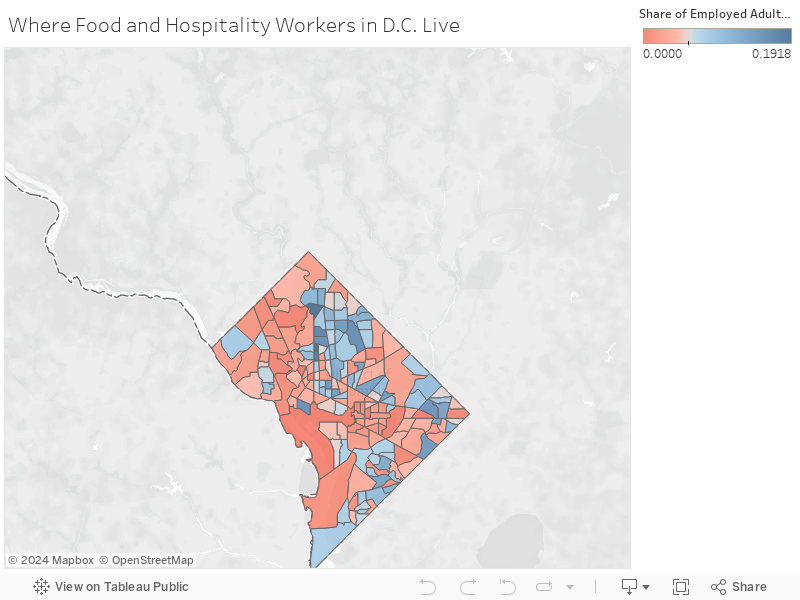

Across the district, 5.8% of all employed adults are food or hospitality workers, but those workers aren’t even concentrated throughout the city. In the average precinct that voted ‘Yes’ for the Initiative, 6.7% of employed adults are food or hospitality workers, compared to only 3.5% in those that voted ‘No’.

Perhaps not surprisingly, the precincts with the lowest level of support for Initiative 77 are the ones where voters are very unlikely to have a neighbor who relies on tips. In Precinct 5, home to Georgetown Cupcake, only 1% of employed adults are food or hospitality workers — and only 37% of voters said ‘Yes’ to Initiative 77, the lowest rate of any precinct in the district. Virtually none of the cities’ food and hospitality workers live in the Potomac-facing western neighborhoods voting ‘No’ to raise the tipped minimum wage.

All 29 precincts where more than 10% of employed adults are food or hospitality workers voted ‘Yes,’ like Precinct 120, near the Congress Heights Metro Stop in Southeast D.C., where 74% of votes were to pass Initiative 77.

Recalling her experiences working at Hot Shoppes as a waitress in Washington D.C. in 1970, Angie Whitehurst of Ward 4, now a StreetSense vendor, described the barriers facing tipped workers, who make an average wage of $14.41 an hour including tips according to the Economic Policy Center. “Most tipped workers do not have the benefits that the top 1% in this city have. If they take a day off, that’s a day without pay. It costs too much money just to take the bus to and from work,” Whitehurst said. “It’s an unlivable wage, and it’s like gambling.”