While popular, Tide Pods are staggeringly dangerous for young children and people with disabilities.

Proctor and Gamble launched the Tide Pods in 2012. In 2011, 2,862 children were hospitalized because of laundry-detergent related injuries. In 2013, that number was triple: 9,004 children were driven to hospitals by laundry detergent.

The problem isn’t that Tide Pods are uniquely toxic, or contain chemicals never used before. The problem is that they’re cute. They’re colorful. And they’re small. It’s the good things about Tide Pods that we have to change to make them safer.

What Tide Pods teach us about consumer product safety is that it’s not always the “bad parts” of products that make them risky: products aren’t always risky because of a gear that breaks and causes an accident, faulty wiring, or a toxic ingredient. Tide Pods drove children to the hospital not because they had more bad parts than other detergents, it’s because they had more good parts: they looked better and felt better. A bill put forth in the New York State Assembly would force detergent packets sold to be in “opaque, uniform colors” — unlike the squishy, candy-like, blue-white-and-orange Tide Pods sold today. Seems like a good thing to me: changing the color scheme may make the product less popular, but won’t make the product any less effective.

To help get Americans out of debt, regulators need to force banks to make their financial products less like squishy, colorful candy. We need ugly detergent that is just as good at cleaning clothes but poisons fewer children. We also need financial products that are equally good at helping families navigate a challenging economy but that tap into fewer of our weaknesses and biases.

Despite a handful of useful credit card regulations passed in 2009, too high of a percentage of Americans paychecks still get lost to loan interest and fees. While student loan debt dominates the news cycle, more American families hold credit card debt than any other form of loan: roughly half of all Americans carry an interest-bearing balance on credit cards. Last year, Americans paid more than $104 billion in credit card fees and finance charges: an average of $823 per American family. In the face of unstable and low-paying jobs, credit cards and other consumer lending products can sometimes help families plug goals and pay gaps, but clearly turning over $823 from American paychecks to big banks ultimately makes the problem worse.

Credit limit increases and credit card rewards are two “features” that make credit cards dangerous — and both “features” could be regulated in ways that wouldn’t make it harder for the Americans who actually face short term borrowing needs.

Banks should be required to get the customer’s permission before raising their credit limit.

Imagine you’re on a diet and you’re trying hard to cut back on sweets. Many of us find it hard to turn down the plate of cookies sitting out in the break room, even if we’d be unlikely to go down the block to buy dessert. Similarly, for the many Americans struggling to make ends meet, a high credit limit is an unwanted invitation to take on debt they know will cause stress and heartache. Researchers Scott Schuh from the Federal Reserve Bank of Boston and Scott L. Fulford of Boston College found that for Americans who borrow money on their credit cards “nearly 100% of an increase in credit limits eventually becomes an increase in debts.” There’s a huge psychological difference between applying for a new loan versus using credit that’s already available on a credit card you have. You might not apply for a new loan to go to your cousin’s wedding, even if you’d charge it to an existing card without knowing when you’ll pay it back. Moreover, too many consumers think of the credit limit as the amount banks think they can ‘safely afford’ to borrow.

The U.S. regulatory framework says a high credit limit is a good thing, implying issuers shouldn’t need your permission to raise your credit limit, but a quick scan of Twitter reveals that many consumers feel different when they say things like: “Got an email that my credit limit has been raised and that is so dangerous how do I decline ” If customers had to request credit limit increases they actually wanted, instead issuers raising customer credit limit without customers prior consent, a high unused credit line wouldn’t be looming over so many Americans heads as an unwanted temptation to enter a debt trap. Australia and the United Kingdom are both good case studies here. Australia prohibits banks from raising credit limits except at the customer’s request, and in the United Kingdom, banks can’t raise the credit limits of people who haven’t been able to repay their card balance in full at least once over the last year.

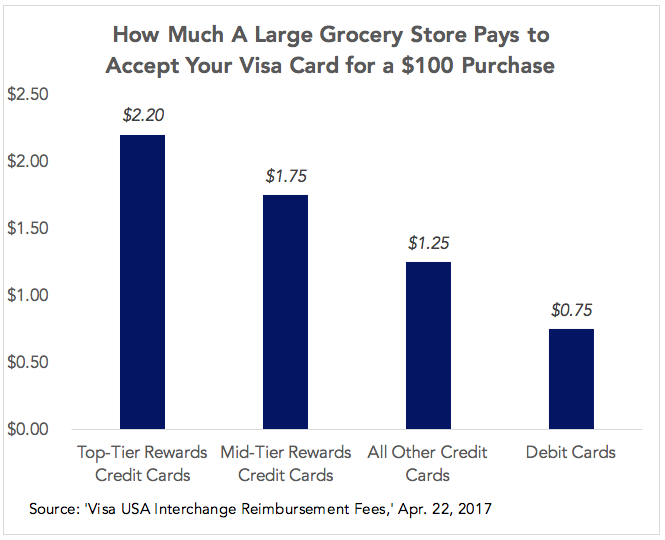

Credit card rewards are another trojan horse. For some consumers of course, the airline miles or cash back is huge boon — there’s no doubt that for Americans who pay their bill in full every month, getting 1% or 2% back on purchases is a nice perk. But Schuh has shown that to cover the cost of these rewards, banks have to charge high “interchange” fees to merchants, which in turn result in higher prices for consumers. Perhaps more importantly, credit card rewards make it even more tempting for people to spend money they don’t have. The European Union and Australia have both capped these credit card processing fees charged to merchants, which effectively eliminated rewards credit cards in those countries. And good riddance. Simpler products with fewer distinct terms make it easier for people to select the lowest cost option: consumers would find it easier to identify the lower-interest-rate cards if they weren’t also benchmarking the value of airline miles. And there’s no reason low-income Americans who don’t qualify for credit cards to begin with should pay higher prices at merchants to allow wealthy Americans with Chase Sapphire Reserve cards can fly first class to Japan.

While payday lenders charge exorbitant rates and fees, the one thing you can say in defense of payday loans is that they are typically used by people who are explicitly conscious of the fact they’re borrowing money, and are aware it’s not going to be cheap. By contrast, credit cards are slippery, intractable instruments in a country where only 38% of jobs pay enough for people to afford a middle class life, and living within your means can be a constant struggle. Occasionally borrowing on a credit card is the right answer for a family: economists Kyle Herkenhoff and Gordon Phillips have found that unemployed Americans with more credit card liquidity are able to extend their job searches by putting bills on their credit card, ending up with higher paying jobs as a result. But many Americans come to find that despite their irregular income or unexpected expenses, using a credit card to smooth things over just makes their budget shortfalls more and more severe as time passes. Ending unsolicited credit limit increases and taking steps to curb credit card rewards wouldn’t limit Americans from accessing credit when they need it — unlike capping credit card interest rates, as Bernie Sanders and Alexandria Ocasio-Cortez have proposed, which would undoubtedly increase how many Americans get declined when they apply for new credit.

By going after some of the seemingly attractive features of credit cards, we can make them less like multicolored detergent pods, and stop the banks from taking Americans to the cleaners.